October 14, 2025

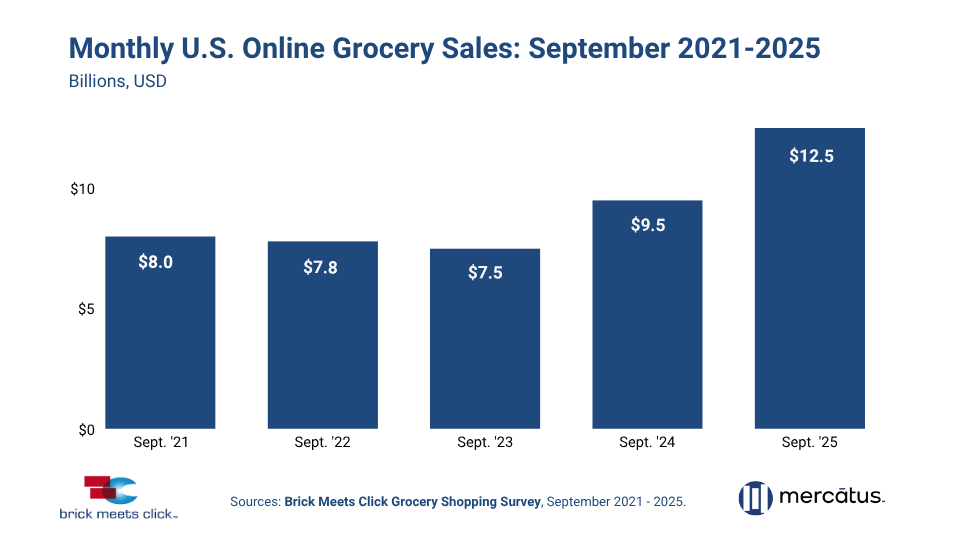

September 2025 eGrocery Sales Jump 31% Versus Year Ago to $12.5 Billion

No items found.

Search by topic

U.S. online grocery sales have soared to unprecedented levels, hitting a new high of $12.5 billion in September 2025. This marks a significant 31% increase over the previous year and is the second consecutive month a new record has been set, according to the Brick Meets Click Grocery Shopper Survey, sponsored by Mercatus.

This explosive growth was fueled by three primary factors:

- The largest base of monthly eGrocery shoppers to date.

- Continued gains in order frequency.

- Strong spending per order (i.e. average order value).

Online spending captured its highest share of weekly grocery spending since the very beginning of the pandemic, jumping 400 basis points (bps) versus last year to nearly 19% in September 2025. This is the second-highest contribution level recorded for eGrocery, only behind May 2020.

Deep Dive into the Growth Drivers

1. Expanding Shopper Base (MAUs)

- The overall base of eGrocery Monthly Active Users (MAUs) reached a new high in September 2025, up nearly 13% year-over-year (YOY).

- The majority of this increase came from re-engaging less frequent customers who last purchased groceries online two to three months prior.

- All three receiving methods—Delivery, Pickup, and Ship-to-Home—posted gains in their MAU bases versus last year, with Delivery setting a new high.

- All age groups reported more MAUs YOY, with the 60+ age group contributing almost half of the YOY gains.

2. Increased Order Frequency

- The average number of online orders per MAU climbed 9% versus a year ago. This marks the 13th consecutive month of YOY gains in frequency.

- This increase was driven by a jump in the share of MAUs completing three or more online orders during September.

- Small Metro markets posted the strongest relative gains in frequency, climbing at a rate nearly twice that of other market types.

3. Higher Average Order Value (AOV)

- The combined AOV for Delivery and Pickup grew by almost 8% YOY.

- Gains were recorded across Supermarket, Mass, and Dollar formats, with larger surges in spending per order at Hard Discounters and Club stores.

- Ship-to-Home’s AOV finished up by nearly 11% YOY, primarily fueled by Amazon's pure-play services and its ongoing expansion of same-day fresh grocery.

Implications for Regional Grocers: In-store & competitor challenges

While online sales surge, online growth continues to negatively impact the performance of in-store sales. From January through September 2025, in-store sales growth YOY slowed to under 1.5%, compared to 3.0% during the comparable 2024 period.

In addition, cross-shopping is becoming a significant challenge for regional grocers.

- There has been a sharp increase in the share of Grocery MAUs that also completed at least one eGrocery order with Mass retailers during September, versus the two prior years.

- Cross-shopping rates with Walmart continued to expand significantly in 2025.

- The rate for Target also increased YOY, although it remains significantly lower than Walmart.

In summary, the September 2025 data underscores the accelerating shift of grocery spend online, driven by an expanding, more engaged, and higher-spending user base across all age groups and receiving methods.

CPG brands and retailers must adapt strategies to capture their share of the rising AOV in Delivery/Pickup and Ship-to-Home, while regional grocers must urgently address the growing challenge of cross-shopping with Mass retailers, and more specifically Walmart.

About this consumer research

The Brick Meets Click Grocery Shopping Survey is an ongoing independent research initiative created and conducted by the team at Brick Meets Click and sponsored by Mercatus.

Brick Meets Click conducted the most recent survey on September 28-30, 2025, with 1,493 adults, 18 years and older, who participated in the household’s grocery shopping, and a similar survey in September 2024 (n=1,740). Results are adjusted based on internet usage among U.S. adults to account for the non-response bias associated with online surveys. Responses are geographically representative of the U.S. and weighted by age and income to reflect the national population of adults, 18 years and older, according to the U.S. Census Bureau.

Insight-driven advocacy for Grocery

retail success.

© 2026 Brick Meets Click - all rights reserved - unauthorized use prohibited.